Paul, Weiss is an acknowledged leader among U.S. law firms representing Canadian public and private companies and their underwriters. With almost 50 years of history in Canada and an office in Toronto, our vibrant Canada practice is the largest among U.S. law firms and reflects our long-standing commitment to our clients in their Canadian–U.S. cross-border matters.

Q1 2025 U.S. Legal & Regulatory Developments

April 17, 2025 Download PDF

The following is our summary of significant U.S. legal and regulatory developments during the first quarter of 2025 of interest to Canadian companies and their advisors.

1. Significant Delaware Corporation Law Amendments Enacted

On March 25, 2025, Delaware Governor Matthew Meyer signed into law significant changes to Sections 144 and 220 of the Delaware General Corporation Law (“DGCL”). After vigorous debate, the amendments were approved by significant majorities in both houses of the Delaware General Assembly in substantially the form proposed by the sponsors of the bill, after the Delaware General Assembly received input from the Corporation Law Section of the Delaware State Bar Association. These amendments aim to provide greater clarity and predictability in structuring controller and other interested transactions, and to reduce undue burdens on corporations by modifying the standards applicable to stockholder access to corporate books and records. Our view is that these statutory amendments are highly beneficial to Delaware corporations and their stockholders.

Key amendments include:

- Implementing a statutory safe harbor to provide liability protection for controller/interested transactions that comply with more straightforward, specified procedures. For controlling stockholder going-private transactions to qualify for the safe harbor, the procedures are a modified MFW framework, requiring approval by both (i) a committee of directors determined to be independent by the board, and (ii) a majority of the votes cast by disinterested stockholders. Non-squeeze-out transactions with controlling stockholders and other interested transactions would have to satisfy only one prong of this framework to qualify for the safe harbor.

- Defining “controlling stockholder” as a stockholder that (i) owns a majority in voting power; (ii) owns at least one-third in voting power and exercises managerial authority; or (iii) otherwise has sufficient voting power or rights to control the board.

- Adding more rigorous standards governing stockholder demands to inspect corporate books and records, including modifying the requirements for what constitutes a proper demand, narrowing the books and records accessible to stockholders upon a proper demand and imposing heightened evidentiary standards for obtaining non-formal books and records such as emails and text messages.

The amendments became effective on March 25, 2025 and apply retroactively, except for actions or proceedings completed or pending, or demands to inspect books and records made, on or before February 17, 2025.

For the full text of our memorandum, please see:

For the full text of our memorandum discussing the amendment as proposed in February 2025, please see:

For the full text of the amendments to Section 144 and 220 of the DGCL, please see:

2. SEC Developments

Prior to the confirmation of Paul Atkins by the U.S. Senate on April 9, 2025, new developments were already occurring at the U.S. Securities and Exchange Commission (the “SEC”).

Former SEC Chair Gary Gensler and Commissioner Jamie Lizárraga stepped down in January, leaving just three Commissioners at the SEC’s helm (Mark Uyeda, Hester Peirce and Caroline Crenshaw). In the interim, Commissioner Uyeda was named as Acting Chair of the SEC, and commenced redirecting the SEC’s agenda.

Mr. Atkins has publicly advocated against “regulation for regulation’s sake,” regulation by enforcement, excessive penalties against public corporations and overreach by the SEC in excess of its legislative mandate, and promoted regulatory standards for cryptocurrencies. We expect to see these themes in an Atkins-led SEC. Recent SEC developments may serve as a preview of what we can expect, given that former Acting Chair Uyeda and fellow Commissioner Peirce each served as counsel to Paul Atkins when he was a Commissioner.

Facilitating Capital Formation

Former Acting Chair Uyeda announced that he directed SEC Staff to review a number of rules (and proposals) with a focus on facilitating capital formation, including:

- the implementation of recommendations from the SEC’s Office of the Advocate for Small Business Capital Formation regarding the exempt offering regime (including Regulation CF) to improve capital raising opportunities for entrepreneurs;

- enabling greater retail investor participation in the private markets (including changes to the accredited investor definition and to permit retail investing via pooled vehicles);

- potential changes to the “emerging growth company” definition and extending the disclosure compliance “on-ramp” that accompanies emerging growth company status;

- whether to re-align the Commission’s filer categories (large accelerated filer, accelerated filer, non-accelerated filer, smaller reporting company) to reflect the size and makeup of public companies today (the definitional have not been indexed for inflation); and

- the disclosure requirements applicable to each filer category (in particular, former Acting Chair Uyeda noted that he had asked SEC Staff to “identify rules that should apply only to the largest companies”).

Expansion of Nonpublic Review of Registration Statements

In addition, with a view to facilitating capital formation, on March 3, 2025, the SEC announced that it was expanding the circumstances under which registrants could submit draft registration statements to be reviewed on a nonpublic basis by the SEC. As a result,

- issuers may now also submit draft registration statements to initially register securities pursuant to Section 12(g) of the Securities Exchange Act of 1934 (the “Exchange Act”) on Forms 10, 20-F or 40-F for review on a non-public basis (previously only registration statements submitted under the Securities Act of 1933 (the “Securities Act”) or Exchange Act Section 12(b) were eligible);

- issuers may submit draft registration statements for offerings no matter how long they have been a public company (previously issuers could only submit registration statements on a draft basis within the first 12 months that they were a public company);

- issuers will still be required to file the registration statement and nonpublic draft submission at least 2 business days prior to the effective time;

- the SEC will continue to review only the initial submission on a nonpublic basis and issuers filing an amendment to respond to SEC comments will need to do so publicly;

- de-SPAC registration statements may be submitted on a draft basis for nonpublic review if the co-registrant target would otherwise be independently eligible to submit a draft registration statement; and

- issuers may omit the names of underwriters from their initial submissions.

Cryptocurrency

On January 21, 2025, former Acting Chair Uyeda announced that the SEC had launched a Crypto Task Force. Led by Commissioner Peirce, the goal of the Task Force is to develop a comprehensive and clear regulatory framework for crypto assets. The announcement signaled a change in enforcement priority (the Task Force will help the Commission “deploy enforcement resources judiciously”). Public input may be submitted to the Task Force at Crypto@sec.gov.

On January 23, 2025, the SEC Staff rescinded Staff Accounting Bulletin No. 121, which had effectively prevented banks and broker-dealers from taking custody of crypto assets.

On February 27, 2025, the SEC’s Division of Corporation Finance issued a statement that meme coins are not securities and the offer and sale of meme coins does not require registration under the Securities Act (or an exemption therefrom).

On February 27, 2025, the SEC announced it had filed a joint stipulation with Coinbase Inc. and Coinbase Global Inc. to dismiss the SEC’s civil enforcement action against the two entities. In addition, Robinhood Markets, Inc., OpenSea and Kraken have recently announced that the SEC’s investigations into their respective failures to register crypto tokens as securities have been closed. These announcements herald a major shift in crypto enforcement.

On March 21, 2025, the SEC’s Crypto Task Force held its first public meeting with experts, discussing whether cryptocurrencies will require a separate regulatory framework that differs from the approach the SEC takes overseeing securities such as debt or equities.

Tender Offers and Share Registration in Business Combinations

On March 6, 2025, the SEC staff (the “Staff”) issued new and amended compliance and disclosure guidance related to tender offers and the registration of shares in business combinations. The new guidance notes that an extension of a tender offer for less than 5 business days may be adequate under certain circumstances. The guidance also addresses whether certain events constitute material changes requiring an extension of the offer period, with specific guidance on financing changes and the substitution of funding sources. Finally, the guidance clarifies that the Staff will not object to the registration of acquirer securities on Form S-4 in Rule 145(a) transactions in circumstances where certain target shareholders have executed lock up agreements or delivered vote consents in advance of a registration statement filing, provided certain conditions are met, including the delivery of a prospectus to all target security holders entitled to vote.

Climate

In March 2024, the SEC adopted final climate disclosure rules. The rules quickly became the subject of numerous legal challenges, which have been consolidated into one litigation in the Eighth Circuit. In April 2024, the SEC issued an order staying its recently adopted climate-related disclosure requirements pending the outcome of litigation.

On February 11, 2025, former Acting Chair Uyeda issued a statement announcing that he had directed Commission Staff to notify the Eighth Circuit of the changed circumstances and request that the Court not schedule the case for argument to provide time for the SEC to “deliberate and determine” appropriate next steps.

Short Sale Reporting

In October 2023, the SEC adopted rules requiring institutional investment managers with short positions that exceed certain reporting thresholds to confidentially disclose those positions and net monthly activity within 14 days of the end of every month on new Form SHO. Compliance with these requirements commenced January 2, 2025, and the first Form SHO filings would have been due February 14, 2025.

On February 7, 2025, the SEC issued an order granting a 12-month exemption from compliance with its short sale disclosure requirements. As a result of the SEC’s order, compliance will be required commencing January 2, 2026, and the first Form SHO filings will be due February 17, 2026.

Nasdaq Board Diversity Rules

In August 2021, the SEC approved Nasdaq’s board diversity requirements, which required listed companies to (i) disclose the voluntarily self-identified diversity characteristics of their board members and (ii) have, or explain why they do not have, at least one director who self-identified as a female, an underrepresented minority or LGBTQ+ and, beginning in 2025, at least two self-identified diverse directors.

On December 11, 2024, in Alliance for Fair Board Recruitment v. SEC, the Fifth Circuit struck down Nasdaq’s board diversity disclosure requirements, holding en banc that the SEC had exceeded its authority in approving them. The challenge was initially unsuccessful, with a Fifth Circuit panel upholding the requirements in 2023. On February 4, 2025, the SEC approved Nasdaq’s amendment to remove these requirements from its listing rules.

For the full text of our memorandum, please see:

3. Update on Antitrust Enforcement

Merger Enforcement

- New HSR Premerger Notification Rules Go into Effect. On February 10, 2025, the new more onerous Hart-Scott-Rodino (“HSR”) premerger notification rulesbecame effective. Chairman Ferguson endorsed the updated rules, writing that they “will allow us to find anticompetitive mergers efficiently, while more quickly getting out of the way of deals that will benefit the American people” and that they “were long overdue.” The rules remain subject to a pending court challenge. A resolution of disapproval under the Congressional Review Act, which, if passed, would nullify the new rules, has been introduced in Congress.

According to Federal Trade Commission (“FTC”) Chairman Ferguson, the Premerger Notification Office (“PNO”) received a wave of filings made under the old rules in the run-up to the effective date. Whereas in a typical week there are “between 35 and 50 transactions” notified, in the week before the new rules became effective, the PNO “received 394 filings accounting for about 200 transactions.” Premerger notification filings, which can be made on the basis of a letter of intent, start the clock on the HSR waiting period that parties must observe before closing. The waiting period for the last of the deals subject to the old rules filed on February 7, 2025 before 5 p.m. expired on March 10, 2025 at 11:59 p.m. The acceleration of filings to take advantage of the old rules likely means that there were far fewer filings than normal submitted in the first few weeks under the new rules, especially given the onerous burdens and extra time now required to prepare HSR notifications. This may give the agencies some breathing room to work through the surge of filings. - Early Terminations of HSR Waiting Period Resumed. Now that the new rules are in effect, the FTC has resumed early terminations of the waiting period for certain transactions that do not raise competitive issues (as determined by the agencies).

- 2023 Merger Guidelines Remain in Effect. On February 18, 2025, Chairman Ferguson endorsed the continued use of the 2023 FTC-DOJ Merger Guidelines. In a memoto FTC staff, the chairman cited the benefit of “stability” and the resource cost of “wholesale recission and reworking of guidelines.” He wrote that, while they may not be “perfect,” the new guidelines are a “restatement of prior iterations of the guidelines, and a reflection of what can be found in case law.” The then-acting assistant attorney general of the U.S. Department of Justice (“DOJ”) Antitrust Division also endorsed the continued use of the new guidelines, citing comments by assistant attorney general Abigail Slater at her confirmation hearing that she will “follow the legal and economic framework described in the” new guidelines.

We note that this does not mean that the agencies will pursue every theory of potential competitive harm described in the guidelines at every turn. However, courts have thus far favorably cited aspects of the guidelines. Indeed, the courts in the IQVIA-DeepIntent, Kroger-Albertsons and Tapestry-Capri matters all cited the market concentration thresholds in the new guidelines in determining that each of these deals was likely to harm competition. (It should be noted, however, that a read of these opinions suggests that the same conclusions would have been reached had the courts used the higher thresholds in the prior guidelines.) - Merger Remedies Are Back in the Mix. The agencies may once again be willing to settle merger matters with divestiture remedies. DOJ Antitrust Division head Abigail Slater said at her confirmation hearing that “often remedies, if done right, if they're robust divestitures, for example, can remove any competitive harm from a merger in order to allow it to proceed in a pro-consumer, pro-competitive manner.” In a speechin January, FTC Commissioner Melissa Holyoak said: “Where a divesture can successfully preserve lost competition from the underlying merger, the agencies should consider it, and should focus on the potential benefits to innovation from the remainder of the merger.”

- Will the FTC Limit the Use of Prior Approval Provisions in Consent Orders?It remains to be seen whether the FTC will continue routinely to require prior approval provisions in consent orders resolving merger matters, as was the policy in the prior administration. These provisions generally require parties to obtain approval from the FTC prior to closing future transactions involving the same relevant market, and have the potential to cause deal uncertainty and indefinitely delay parties’ ability to close a deal.

For the full text of our memorandum, please see:

4. Treasury Department Announces Suspension of Corporate Transparency Act Enforcement for U.S. Entities or Their Beneficial Owners; Proposes New Limited Scope for Requirements

On March 2, 2025, the Department of the Treasury (the “Treasury”) announced that it will (i) “not enforce any penalties or fines associated with the beneficial ownership information reporting rule (the “BOI Reporting Rule”) under the existing regulatory deadlines” and (ii) will be issuing a “proposed rulemaking that will narrow the scope of the rule to foreign reporting companies only.” Under the new rule, the Treasury will “not enforce any penalties or fines against U.S. citizens or domestic reporting companies or their beneficial owners after the forthcoming rule changes take effect.”

For the full text of our memorandum, please see:

For the Treasury’s March 2, 2025 announcement suspending enforcement of the Corporate Transparency Act against U.S. citizens and Domestic Reporting Companies, please see:

For FinCEN’s interim final rule, please see:

5. FCPA Enforcement Paused After DOJ Day-One Directives Announce Significant Shift in Priorities, Including the Reorientation of FCPA, FARA and Money Laundering Enforcement

On February 10, 2025, the White House issued its Executive Order Pausing Foreign Corrupt Practices Act (“FCPA”) Enforcement to Further American Economic and National Security requiring a 180-day pause on all new FCPA investigations or enforcement actions, as well as a review of all existing FCPA matters. During the pause, which can be extended for an additional 180 days, the Attorney General is required to issue FCPA enforcement guidelines for future cases, all of which must be approved by the Attorney General. The Executive Order also calls for a retrospective review of prior FCPA investigations and enforcement actions.

The Executive Order expresses the view that prohibitions on bribery undermine the competitiveness of U.S. companies abroad. As explained in the “Fact Sheet” accompanying the Executive Order: “U.S. companies are harmed by FCPA overenforcement because they are prohibited from engaging in practices common among international competitors, creating an uneven playing field.” Both the Executive Order and Fact Sheet also state that the FCPA undermines “American national security” because it thwarts companies from gaining “strategic business advantages” aboard.

Key Takeaways

Regardless of whether the Executive Order and the new directives have a long-term impact on enforcement activity in these areas, they do contain important pronouncements. Companies should consider the following potential implications of these new policies:

- Companies should take a close look at their compliance programs, including their know-your-customer and third-party risk management practices, to ensure that they are addressing cartel and Transnational Crime Organization (“TCO”) risks. Counterparty risk management processes, including due diligence, engagement and monitoring practices may need to be adjusted to account for these risks. Some cartels and TCOs, along with their leadership, already appear on sanctions lists maintained by OFAC, which will be helpful for companies that already incorporate sanctions screening in their compliance programs.

- These latest shifts in enforcement priorities are not a safeguard against investigation or prosecution for corruption or money laundering-related offenses. As a result, companies are cautioned against any de-investment in compliance programs or related controls in light of these latest developments.

- The statute of limitations for most federal crimes is five years (six years for certain FCPA offenses, ten years for bank fraud), meaning relevant offenses that occurred in the recent past or during the current administration could be prosecuted by a subsequent administration. Moreover, prosecutors in the early stages of investigations frequently request—and receive—tolling agreements, or obtain court tolling orders based on requests for foreign evidence, which allow the DOJ (as well as the SEC) to bring enforcement actions for conduct that occurred much earlier in time.

- While temporarily frozen, FCPA investigations that were in motion prior to February 10th—some known to the subjects of the investigation, and some unknown—may ultimately proceed on track following the Attorney General’s review of those cases, regardless of whether they have a cartel/TCO nexus.

- The DOJ’s shift in priorities does not extend to other federal regulators, including the SEC, which has its own FCPA Unit to investigate and prosecute violations of the FCPA’s anti-bribery and internal accounting provisions involving issuers, and the Commodity Futures Trading Commission, which has brought several foreign bribery actions under the Commodities Exchange Act. The Executive Order’s discussion of the foreign affairs, economic and national security prerogative of the President, however, suggest that civil enforcement actions by the SEC or other federal regulators may also be impacted.

- Various state authorities, especially State Attorneys General from Democratic states, may seek to fill the enforcement void and, to the extent there is state legislation and a sufficient jurisdictional hook, investigate companies for misconduct that has traditionally been the province of federal regulators. We may also see an uptick in transnational bribery cases from select local prosecutors such as the Manhattan District Attorney’s Office, which has a history of pursing complex, cross-border financial crime, and may similarly shift more attention to foreign bribery.

- The DOJ’s directives may draw resources from enforcement areas not directly tied to cartel or TCO activity. For example, the shift in priorities could reallocate the DOJ’s FCPA-focused resources, which, in contrast to the DOJ’s Narcotics-, MLARS- and Violent Crime and Racketeering Section-focused resources, historically have not been used to target cartel and TCO-related activity. Similarly, DOJ enforcements efforts related to kleptocracy, sanctions and money laundering that do not involve cartels or TCOs may be less of an emphasis in the new administration. However, as we have noted, even if there is some resource reduction, that may be counterbalanced by other circumstances and developments which could help DOJ maintain its impact in these enforcement areas.

- Finally, companies should not assume that the DOJ will drop existing investigations following its review, nor should they assume that significant conduct not falling clearly within the newly-articulated priorities will not be investigated.

For the full text of our memorandum, please see:

6. Record HSR Gun-Jumping Fine Focuses Attention on Interim Operating Covenants

In a January 7, 2025 HSR enforcement action, the DOJ obtained a record $5.6 million civil penalty from companies accused of violating pre-merger “gun-jumping” prohibitions.

Under the Hart-Scott-Rodino Antitrust Improvements Act of 1976 (“HSR Act”), parties must report to the FTC and Antitrust Division of the DOJ proposed acquisitions of assets, voting securities or certain noncorporate interests if certain transaction and party size thresholds are met and an exemption does not apply.

Notifiable transactions are subject to a statutory waiting period, typically 30 days, which gives the antitrust agencies time to undertake a preliminary assessment the potential competitive effects of proposed transactions. The parties cannot close and the buyer cannot direct the business operations or otherwise exercise beneficial ownership of the target until the waiting period expires or is terminated. Violations of the notification and waiting period requirements of the HSR Act are subject to annually adjusted civil penalties for each day of noncompliance. The maximum daily penalty is currently $51,744.

The U.S. antitrust agencies have long had the view that when a buyer gains operational control of the target’s ordinary course business decisions before expiration of the HSR waiting period, it is gun jumping in violation of the HSR Act. Depending on the circumstances, inappropriate buyer-target pre-merger coordination could also give rise to liability under section 1 of the Sherman Act, which prohibits conspiracies in restraint of trade.

The DOJ’s complaint against the buyers (Verdun Oil and its sister company XCL Resources) and target company EP Energy (an alleged XCL competitor) in a now-consummated upstream oil transaction, alleged that certain buyer consent terms in the purchase agreement inappropriately gave the buyers control over the target’s ordinary course business decisions. The purchase agreement contained a provision in the interim operating covenants requiring EP Energy to obtain consent for any expenditures over $250,000. However, according to the complaint, a number of expenditures associated with EP Energy’s ordinary course business decisions—such as purchases of supplies and entering into drilling rig contracts—required outlays of more than $250,000. Therefore, according to the DOJ, the $250,000 threshold gave the buyers the right to control ordinary course business decisions, and they allegedly did so.

In addition to consent rights over certain expenditures, the complaint alleged that the buyers also inappropriately acted to stop EP Energy’s well-drilling activities, control EP Energy’s drilling assets during the interim period, actively manage EP Energy employees and approve routine activities such as hiring field-level employees and contractors. The parties also allegedly coordinated regarding EP Energy’s contract negotiations with customers and upcoming pricing decisions, and shared competitively sensitive information about EP Energy’s business without using appropriate “clean team” safeguards.

This action highlights the importance of careful drafting of interim operating covenants to avoid granting rights to the buyer the exercise of which would constitute gun jumping. It also serves as a reminder that parties should implement and follow an effective antitrust compliance process throughout a transaction’s lifecycle to avoid potential violations of the HSR Act and other antitrust laws governing coordination between independent business entities. Indeed, the complaint serves as a useful antitrust compliance document insofar as it sets out examples of conduct the antitrust agencies see as violating the HSR Act.

This enforcement action demonstrates that parties to a purchase agreement may be subject to substantial civil penalties for gun jumping under the HSR Act, including when post-signing, pre-HSR clearance conduct includes:

- Buyer obtaining or exercising control or consent rights over ordinary course business decisions;

- Buyer assuming target’s contractual obligations and/or the associated financial upside/risk; or

- Buyer obtaining target’s competitively sensitive information without using appropriate “clean team” safeguards.

Special attention should be paid to proposed interim operating covenants that may go beyond preserving the target’s business and value of the transaction and permit the buyer to influence target’s ordinary course business decisions. When negotiating consent rights in interim operating covenants, parties should carefully consider the target’s operations and industry and establish a threshold that is high enough to capture all ordinary course expenditures. Otherwise, they risk running afoul of the HSR Act. Terms that may be appropriate for one industry, may not be inappropriate for another.

For the full text of our memorandum, please see:

For the full text of the DOJ’s complaint for violations of the HSR Act against XCL Resources Holdings, LLC, Verdun Oil Company II, LLC and EP Energy LLC, please see:

7. Shifting Rules of Engagement: The Impact of Recent SEC Guidance on 13G Eligibility, Rule 14a-8 Shareholder Proposals and Exempt Solicitations

The Staff in the Division of Corporation Finance at the SEC has issued three new sets of guidance that may influence and potentially reshape how shareholders engage with companies going forward.

Guidance on 13G Eligibility

On February 11, the Staff issued new compliance and disclosure guidance on the eligibility of shareholders to report their ownership interests on Schedule 13G. The new guidance provides that the Staff’s assessment of a shareholder’s 13G eligibility will consider the subject matter of such shareholder’s engagement with management and the context in which such engagement occurs. A shareholder “who discusses with management its views on a particular topic and how its views may inform its voting decisions, without more, would not be disqualified from reporting on a Schedule 13G.” However, a shareholder who takes the following actions could be disqualified if they:

- recommend that the company remove its staggered board, switch to a majority voting standard in uncontested director elections, eliminate its poison pill plan, change its executive compensation practices or undertake specific actions on a social, environmental or political policy and, as a means of pressuring the issuer to adopt the recommendation, explicitly or implicitly condition their support of one or more of the issuer’s director nominees at the next director election on the issuer’s adoption of its recommendation; or

- discuss with management its voting policy on a particular topic and how the issuer fails to meet the shareholder’s expectations on such topic, and, to apply pressure on management, state or imply during any such discussions that they will not support one or more of the issuer’s director nominees at the next director election unless management makes changes to align with the shareholder’s expectations.

Potential Impact: The Staff’s recent guidance on 13G eligibility may call into question the viability of certain institutional investor stewardship practices. Institutional shareholders have from time to time leveraged their proxy voting power to influence governance practices within companies. Such efforts have been supported by publicly disclosed proxy voting policies and vote bulletins which outline circumstances where an institutional shareholder may vote against directors. In recent years, it has also become an increasingly common practice for stewardship teams to engage with management and directors prior to and following annual meetings to discuss specific matters of concern relating to corporate governance and executive compensation.

As institutional investors look to preserve their Schedule 13G eligibility, there may be changes in the tone, substance and timing of engagements with and communications from stewardship teams. Such changes could make it more difficult for companies to have candid conversations with their key investors on issues of concern. The changes may also make it more difficult for companies to pinpoint the issues that are of priority to their largest investors and are most likely to trigger an adverse vote against directors. As investor priorities and perspectives evolve, companies may also have more difficulty tracking such changes if publicly disclosed proxy voting-related guidance become less frequent or detailed.

The impact of recent guidance changes could be particularly noticeable in contested situations where the perspectives of institutional investors may become more “muted” relative to the views of activist shareholders and proxy advisors who will not be impacted by the latest 13G guidance. In those circumstances, companies could find themselves flying blind if they have not already developed robust relationships with their key investors and strategies to discern their perspectives and the meaning of any indirect messaging. Developing these kinds of robust relationships and strategies can be very useful going forward.

Revised Guidance on Rule 14a-8 Shareholder Proposals

On February 12, the Staff rescinded Staff Legal Bulletin No. 14L (“SLB 14L”), which broadly permitted Rule 14a-8 shareholder proposals relating to “ESG” matters of no economic significance to the target company and issued Staff Legal Bulletin No.14M (“SLB 14M”) in its stead. The adoption of SLB 14M and the recission of SLB 14L mark a direct reversal of policies adopted under former SEC Chair Gary Gensler.

SLB 14M revises guidance on the excludability of Rule 14a-8 shareholder proposals on the basis that a proposal lacks “economic relevance” or is related to the “ordinary business” of a company. Previously, SLB 14L provided that shareholder proposals which lacked “economic relevance” or were related to the “ordinary business” of a company could not be excluded if they concerned a significant social policy matter, regardless of whether such matter was significant to the target company. Going forward, under SLB 14M, the Staff will be taking a company-specific approach and shareholder proponents who raise “social or ethical issues” in their proposal must “tie those matters to a significant effect on the company’s business.” Board analysis on the significance of such matters to a company will also be welcomed again by the Staff to assist in the Staff’s analysis of no-action requests to exclude shareholder proposals.

In addition, new SLB 14M reinstates guidance making it easier for companies to exclude shareholder proposals that seek to “micromanage” them. That “anti-micromanagement” guidance had previously been rescinded by the Gensler Staff’s SLB 14L. The changes signal that the Staff will now be prepared to take a more expansive view on what proposals may be excluded on the basis of “micromanagement.” Amendments to Rule 14a-8 proposed in 2022 but never adopted, and which would have further narrowed the bases for companies to exclude shareholder proposals, have also been placed on hold indefinitely.

Potential Impact: The latest guidance on Rule 14a-8 will make it significantly easier for companies to exclude shareholder proposals from special interest groups with environmental or social agendas. Support for proposals focusing on environmental or social issues have already noticeably declined during the past two proxy seasons as investors weigh the costs and benefits of such proposals.

Special interest shareholder proponents may begin to look to alternative avenues to engage with companies. Over the past year, we have observed social media becoming a platform for pressuring companies on social issues. We have also observed shareholders bypassing the constraints of Rule 14a-8 and turning to Rule 14a-4 to submit multiple shareholder proposals at companies. What is unlikely to happen, however, is an increase in proxy contests relating to non-economic social or environmental issues such as those launched against Starbucks, McDonald’s and Kroger in recent years. Such campaigns are costly, and like shareholder proposals on environmental and social issues, have not gained traction with the broader shareholder base.

While the updated Staff guidance will likely narrow opportunities for shareholders to use Rule 14a-8 shareholder proposals to influence company policy, the appetite for engagement and change among shareholders focused on environmental and social issues has not diminished. Consequently, we may see such shareholders increasingly use third-party engagement platforms or undertake direct outreach to boards and management as part of efforts to influence corporate policy.

Guidance on the Use of Exempt Solicitation Notices

On January 27, the Staff issued new and revised CD&Is for Notices of Exempt Solicitation. Among other changes, the CD&Is:

- require shareholders who own less than $5 million of the class of subject securities and are consequently submitting a voluntary Notice of Exempt Solicitation to clearly state such fact on the cover of such notice;

- require shareholders to disseminate written soliciting materials to security holders before filing such materials under the cover of a Notice of Exempt Solicitation with the Commission;

- reiterate that only written communications that constitute a “solicitation” under the Exchange Act should be submitted under the cover of a Notice of Exempt Solicitation; and

- apply Rule 14a-9, which prohibits materially false or misleading statements, to materials filed under the cover of a Notice of Exempt Solicitation.

Potential Impact: The latest CD&Is on the use of Notices of Exempt Solicitation appear to respond to growing concerns that such notices have inadvertently become a platform for shareholders, particularly shareholder proponents who have submitted Rule 14a-8 shareholder proposals, to engage in “public debate” with companies in the days and weeks leading up to the annual meeting. Unlike Rule 14a-8, which restricts the length of a shareholder’s supporting statement to 500 words, exempt solicitation notices do not impose word count limits. Consequently, for shareholders with limited resources, exempt solicitations have become an attractive avenue to garner the attention of not only the company but also institutional investors and proxy advisors who often review such filings prior to making their voting decisions.

The latest Staff guidance sends a clear signal that the Commission under Chair Paul Atkins will adopt policy positions that are meaningfully more “pro-company” than the approaches pursued under former Chair Gary Gensler. As companies respond to these shifting policies, they would be well advised to ensure that they remain closely attuned to institutional investor expectations given the significant proxy voting influence they continue to wield at many companies.

For the full text of our memorandum, please see:

For the new compliance and disclosure interpretations for Regulation 13D-G, please see:

For the full text of SEC Staff Legal Bulletin No. 14M (CF), please see:

For the new compliance and disclosure interpretations for notices of exempt solicitation, please see:

8. SEC Staff No-Action Letter on Exempt Offerings with General Solicitation Under Rule 506(c)

On March 12, 2025, the Division of Corporation Finance (the “Division”) of the SEC provided new guidance, via a no-action letter, on Rule 506(c) of Regulation D under the Securities Act.

Historically, most issuers conducting exempt securities offerings under Regulation D – including the vast majority of private funds – have done so in reliance on Rule 506(b), which prohibits the use of any “general solicitation or general advertising” in connection with the offering. This has been the case despite the availability, since 2013, of an alternative, Rule 506(c), which permits issuers to engage in general solicitation provided that the issuer and its agents take “reasonable steps to verify” the “accredited investor” status of purchasers in the offering. The vast majority of private fund sponsors and placement agents have chosen not to rely on Rule 506(c) due to (1) the administrative burdens associated with verifying accredited investor status under a non-exclusive list of verification methods expressly permitted under the rule, and (2) the perceived risk that using other, non-specified methods to verify accredited investor status could be challenged, potentially calling into question the validity of the issuer’s offering.

In the new guidance, the Division confirms its view that an issuer conducting a securities offering under Rule 506(c) can reasonably conclude that a purchaser of securities in the offering is an “accredited investor” through a combination of minimum investment amounts and investor self-certifications. Through its clear expression of the Division’s view, the guidance provides an important new path for private funds and other issuers to rely on Rule 506(c), opening the door to more open communication about private fund offerings without the constraints of Rule 506(b)’s prohibition against general solicitation.

New Guidance

Under the new guidance, the Division has confirmed its view that an issuer could reasonably conclude that it has taken reasonable steps to verify the accredited investor status of an investor in a Rule 506(c) offering if:

- There is a minimum investment amount (including binding capital commitments) of:

- for natural persons, at least $200,000;

- for legal entities not formed for the purpose of making the investment, at least $1 million; or

- for legal entities that are formed for the purpose of making the investment or otherwise are accredited investors solely based on the accredited investor status of their equity owners, $1 million, or $200,000 for each of the purchaser’s equity owners if all of the equity owners are fewer than five natural persons; and

- The purchaser provides written representations that:

- they are an accredited investor;

- the minimum investment amount (and, for purchasers that are legal entities accredited solely from the accredited investor status of all of their equity owners, the minimum investment amount of each of the purchaser’s equity owners) is not financed in whole or in part by any third party for the specific purpose of making the particular investment in the issuer; and

- the issuer has no actual knowledge of any facts that indicate that any purchaser is not an accredited investor, or that the minimum investment amount of any purchaser (and, for purchasers that are legal entities accredited solely from the accredited investor status of all of their equity owners, the minimum investment amount of any such equity owner) is financed in whole or in part by any third party for the specific purpose of making the particular investment in the issuer.

For the full text of our memorandum, please see:

For the full text of the SEC’s No Action Letter, please see:

9. Delaware Supreme Court Applies Business Judgment Rule to “Clear Day” Approval of Reincorporation

In Maffei v. Palkon, the Delaware Supreme Court unanimously held that the business judgment rule applies to a corporation’s decision to change its state of incorporation, even if the move arguably favors a controlling stockholder by reducing future liability exposure. The en banc opinion by Justice Karen L. Valihura reverses a Court of Chancery decision holding that entire fairness applied to TripAdvisor’s reincorporation from Delaware to Nevada because the controller received a non-ratable benefit in the form of liability reduction. The Supreme Court explained that, although the more onerous entire fairness standard may be triggered when a corporation re-domesticates to avoid pending or threatened litigation, no such facts were alleged as to TripAdvisor, and “the hypothetical and contingent impact of Nevada law on unspecified corporate actions that may or may not occur in the future” was “too speculative” to justify a departure from the business judgment rule. Companies considering reincorporation to another state would thus benefit from moving on a “clear day” as opposed to when there is live or threatened litigation.

Background

TripAdvisor, Inc. is a Delaware corporation controlled by Liberty TripAdvisor Holdings, Inc. (together, “TripAdvisor”), which is in turn controlled by Greg Maffei. In late 2022 and early 2023, the boards of both TripAdvisor entities considered management presentations about the benefits of converting to Nevada corporations, which purportedly included “greater protection” for directors and officers and a reduction in litigation expenses. The boards approved the conversions in March and April 2023 and sought stockholder approval, which was secured only because Maffei voted in favor of the conversions; otherwise, each measure would have failed.

Stockholder plaintiffs challenged the conversions, which they argued conferred a non-ratable benefit on Maffei and TripAdvisor’s directors. The Court of Chancery agreed, holding that exchanging Delaware law for Nevada law conceivably conferred a material benefit on Maffei and the TripAdvisor directors—reduced litigation risk—that was not shared with TripAdvisor’s stockholders generally, and therefore, Delaware corporate law’s most scrutinizing standard of review, entire fairness, applied. The Court of Chancery declined to block TripAdvisor’s reincorporation with an injunction, but held that monetary damages would be available to the stockholders unless Maffei and the TripAdvisor directors showed that the reincorporation was entirely fair to those stockholders. The Supreme Court accepted TripAdvisor’s interlocutory appeal and reversed the Court of Chancery, holding that the business judgment rule protects Maffei’s and TripAdvisor’s decision to reincorporate in Nevada.

The Supreme Court’s unanimous en banc decision permitting TripAdvisor to change its state of incorporation indicates that the Court is prepared to prioritize the values of “flexibility and private ordering” noted in the opinion, even for entities that have chosen to leave the state. The Palkon opinion also articulates a clearer definition of what counts as a “material, non-ratable benefit,” which will enable transaction planners to better anticipate and account for the types of benefits that may trigger entire fairness review.

For the full text of our memorandum, please see:

For the full text of the Delaware Supreme Court’s opinion, please see:

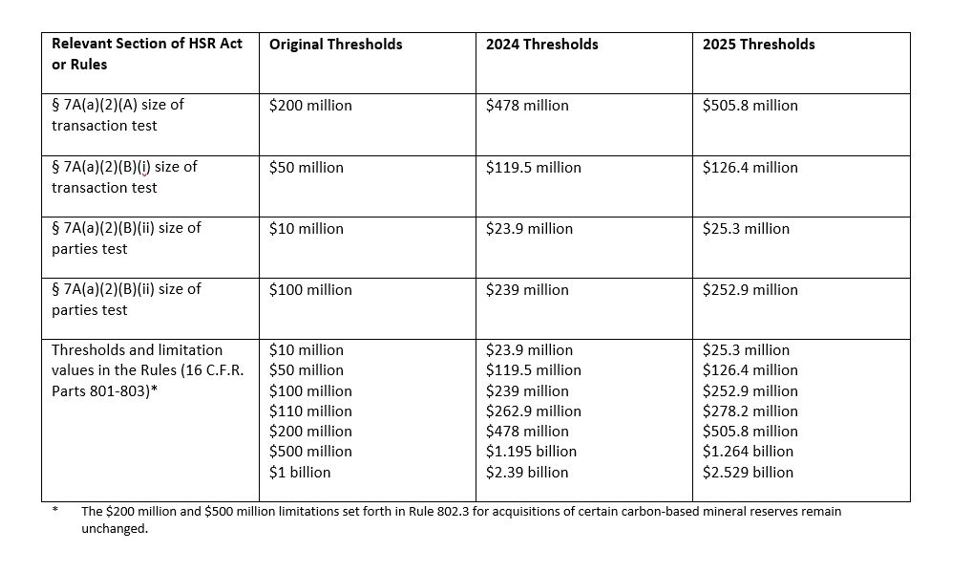

10. Hart-Scott-Rodino and Clayton Act Section 8 Thresholds for 2025

The FTC has revised the jurisdictional and filing fee thresholds of the HSR Act and the Premerger Notification Rules, based on changes in the gross national product (“GNP”) as required by the 2000 amendments to the HSR Act. The filing thresholds and fees increased as a result of the increase in the GNP and apply to transactions going forward (and were applied to all transactions that closed after February 21, 2025). These threshold and filing fee adjustments occur annually and do not alter the HSR filing process. The new HSR rules took effect on February 10, 2025.

The HSR Act requires parties intending to merge or to acquire assets, voting securities or certain non-corporate interests to notify the FTC and the DOJ, Antitrust Division, and to observe certain waiting periods before consummating the acquisition. Notification and Report Forms must be submitted by the parties to a transaction if both the (1) size of transaction and (2) size of parties thresholds are met, unless an exemption applies.

Size of Transaction

The minimum size of transaction threshold which became effective as of February 21, 2025 is $126.4 million, increased from the 2024 threshold of $119.5 million.

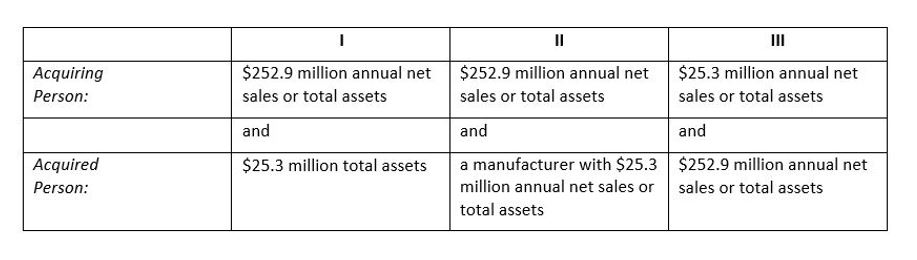

Size of Parties

The size of parties threshold is inapplicable if the value of the transaction exceeds $505.8 million ($478 million in 2024). For transactions with a value between $126.4 million and $505.8 million, the size of parties threshold must be met and will be satisfied in one of the following three ways:

|

The various jurisdictional thresholds, notification thresholds, filing fee thresholds and thresholds applicable to certain exemptions will also increase:

|

Filing Fees

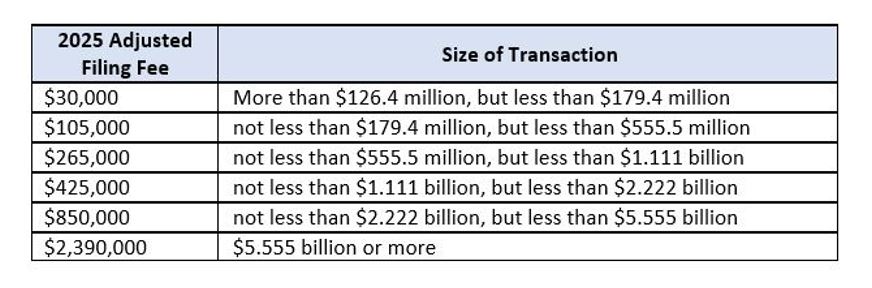

For all filings made as of February 21, 2025, the new HSR filing fees are as follows:

|

The above thresholds and fees will continue to adjust annually.

The FTC also announced the maximum civil penalty for HSR Act violations, raising the amount from $51,744 per day to $53,088 per day, effective as of January 17, 2025.

Finally, the FTC has increased, effective January 17, 2025, the thresholds that prohibit, with certain exceptions, competitor companies from having interlocking relationships among their directors or officers under Section 8 of the Clayton Act. Section 8 provides that no person shall, at the same time, serve as a director or officer in any two corporations that are competitors, such that elimination of competition by agreement between them would constitute a violation of the antitrust laws. There are several “safe harbors” which render the prohibition inapplicable under certain circumstances, such as when the size of the corporations, or the size and degree of competitive sales between them, are below certain dollar thresholds. Competitor corporations are now subject to Section 8 if each one has capital, surplus and undivided profits aggregating more than $51,380,000, although no corporation is covered if the competitive sales of either corporation are less than $5,138,000. Even when the dollar thresholds are exceeded, other exceptions preventing the applicability of Section 8 may be available. In particular, if the competitive sales of either corporation are less than 2% of that corporation’s total sales, or less than 4% of each corporation’s total sales, the interlock is exempt. In addition, Section 8 provides a one-year grace period for an individual to resolve an interlock issue that arises as a result of an intervening event, such as a change in the capital, surplus and undivided profits or entry into new markets.

For the full text of our memorandum, please see:

* * *